MLI Select (Multi-Unit Mortgage Loan Insurance)

CMHC's multi-unit mortgage loan insurance product that rewards landlords/developers who commit to affordability, energy efficiency and/or accessibility with better financing terms (higher loan-to-value/cost, longer amortizations and recourse flexibility). Launched March 7, 2022, replacing MLI Flex. Used for both new construction and acquisition/refinance of multi-unit rental.

What you get

Funding for affordable housing

Who it's for

Owners/developers of multi-unit residential rental properties with a minimum of 5 units (retirement homes require a minimum of 50 units/beds).

This takes you to the official website

What to have ready

Documents they may ask for

- Government ID for everyone in your household, if available

- A copy of your lease or rent agreement

- Recent rent receipt, ledger, or proof of what you owe

- Recent pay stubs, benefit statement, or income proof

- ODSP, Ontario Works, CPP, OAS, or other benefit statement if you have one

- Recent bank statement, if the program asks for it

What to say when you call

“Hi, I found your housing support program and I want to check if I can apply. Can you tell me the current rules, documents needed, and the next step?”

Use the official page first, then call 211 if you are not sure where to start.

Can I get this?

You have a good chance if this sounds like you:

- Non-residential space must not exceed 30% of gross floor area or total lending value

What to do next

Check off each step as you go — we'll remember where you are.

Checkmarks are saved only on this device. We collect nothing.

What the official page looks like

The fine print

More details about the money

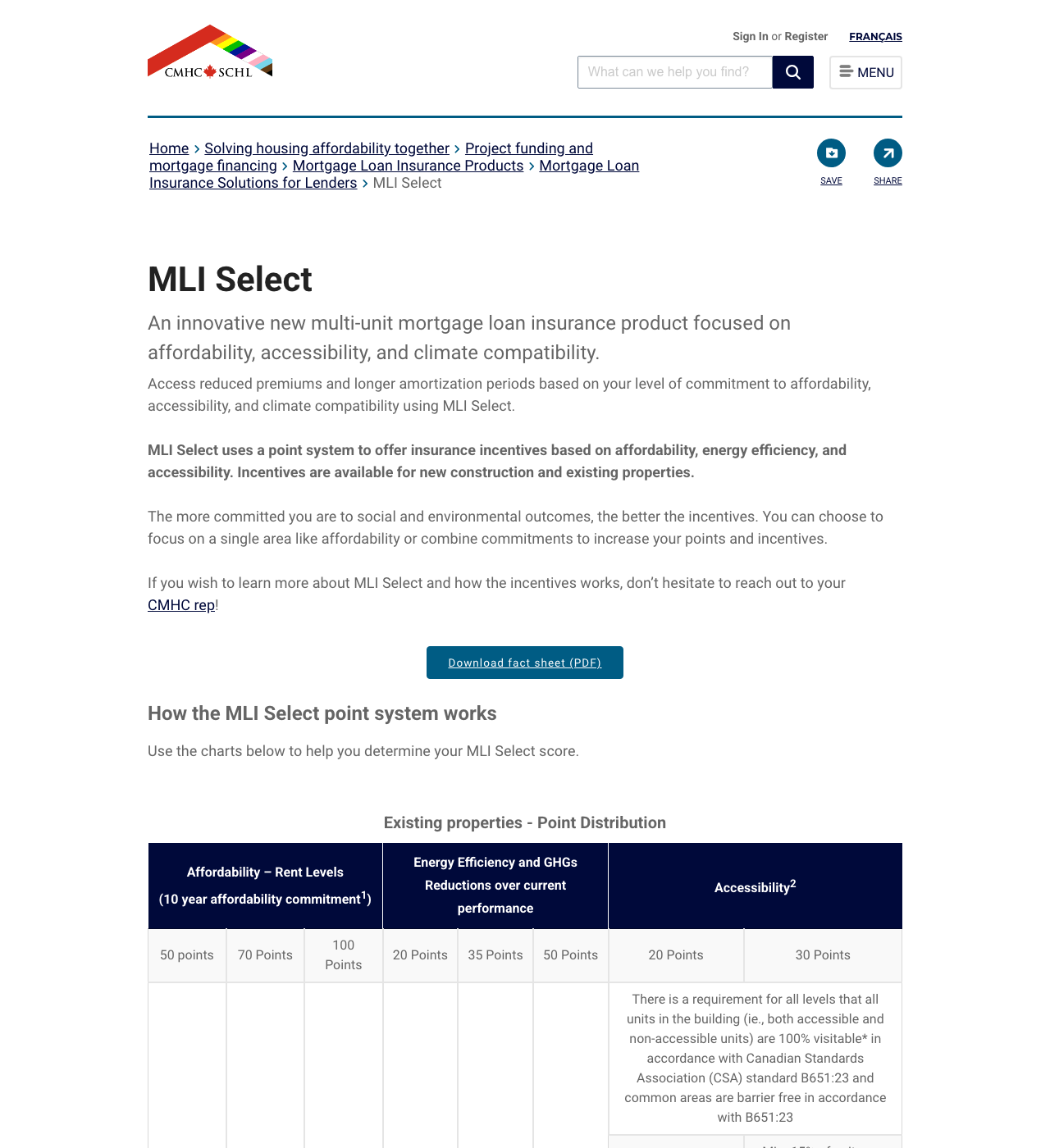

Projects must earn a minimum of 50 points to access MLI Select incentives. Per CMHC's published tiers: minimum 50 points -> up to 85% LTV and up to 40-year amortization (recourse); minimum 70 points -> up to 95% LTV and up to 45-year amortization; minimum 100 points -> up to 50-year amortization with a limited-recourse option. On the affordability pillar, roughly: 50 pts = ~40% of units at 30% of median renter income, 70 pts = ~60% of units, 100 pts = ~80% of units; a 20-year commitment adds bonus points. Premium reductions are set out in CMHC's fee schedules; the borrower does not pay a separate program fee beyond (reduced) CMHC premiums.

Amounts and eligibility change. Confirm the current figure with the program administrator through the official link before you rely on it.

The full eligibility rules

Owners/developers of multi-unit residential rental properties with a minimum of 5 units (retirement homes require a minimum of 50 units/beds). Non-residential space must not exceed 30% of gross floor area or total lending value. Points are earned across three pillars: Affordability (share of units at/below 30% of median renter income, maintained at least 10 years, with bonus points for a 20-year commitment), Energy Efficiency (performance improvement validated by a qualified professional), and Accessibility (accessible units meeting CSA B651 / universal design, with 100% visitability required across all pillars).

Good to know

CORRECTION applied: the draft stated '95% LTV/LTC at 100 points'. The live CMHC MLI Select page maps up to 95% LTV to the 70-point tier; the 100-point tier unlocks up to a 50-year amortization and a limited-recourse option (the most favourable terms), not a higher LTV. 50-point tier = up to 85% LTV / 40-year amortization. Min 5 units (50 for retirement homes) and the 30% non-residential cap are confirmed. CMHC made significant changes in 2024 (including capping energy-efficiency points so projects generally need an affordability component to reach 100 points); exact LTV/amortization/premium values by tier are CMHC's and subject to change. Confirm current criteria and your lender's terms before relying on specific numbers.

Official sources we checked

People also look at

Up to $15,000

Oxford County My Second Unit (Secondary Dwelling Forgivable Loan)

An Oxford County program offering homeowners an interest-free, forgivable loan of up to $15,000 to help plan and finance a secondary, self-contained dwelling unit in their home (e.g.

Up to $45,000

Affordable Rental Housing Program (City of London - Dollars to Doors)

London's incentive that provides up to $45,000 per new affordable rental unit (as a loan) to offset construction costs, in exchange for keeping rents at 80% of CMHC average market rent for at least 25 years.

Up to $3,245/year

Rental Housing Supply Program (Toronto)

Toronto's incentive program for new purpose-built rental housing.